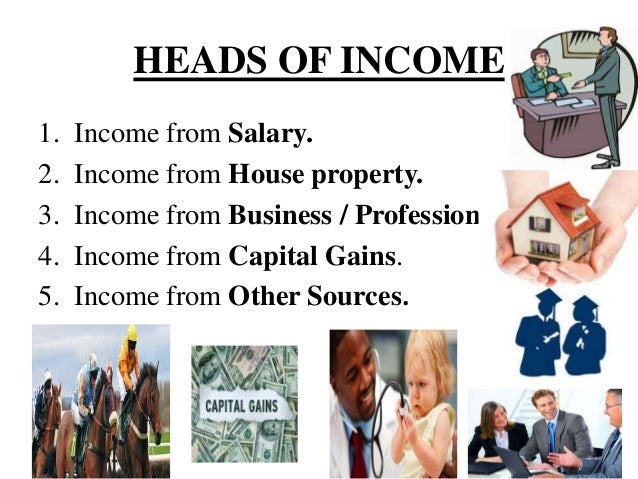

It is absolutely

necessary for a taxpayer to remember that there are several heads under which his

income is divided under the income tax act. The income earned from salary,

house property, profession, business, and capital gains are the main heads under

which taxpayers are supposed to show their earnings. However, there are certain

kinds of income that do not fall under these heads and are categorized under a

separate head called 'income from other sources'. Some of them are completely

taxable and must be mentioned while filing the income tax return if earned.

Failure to do this can lead to imposition of penalty under the Income Tax Act.

Examples of such incomes are as follows:

Image Source: slideshare

Winning lotteries, contests, or games: Sometimes, an individual may win a lottery, a horse

race, or a game of any sort, and unexpectedly get a large amount of money. Any

income thus derived is taxable under the head 'income from other sources'. The

tax rate of 30% (plus 3% cess) is applicable to such an income, irrespective of

the individual's taxability.

Income from dividends: Dividend income: The term 'dividend' is clearly

defined under Section 2(22) of the act. The definition given by this section

covers debentures issued to shareholders, distribution of a certain amount in

case of a company's liquidation, and bonus shares allotted to preference

shareholders. Dividends coming from a domestic company and mutual funds are not

taxed, but dividends coming from a foreign company are taxable under the Income

Tax Act under the head ‘income from other sources’.

Money received as gift from unrelated individual: A sum of money received in excess of Rs. 50,000 by a

person without consideration is taxable. Section 56 (2) of the Income Tax Act

states that gifts from unrelated persons are taxable, including those from

foreign sources and property.

Pension received by heirs of deceased: The amount of pension payable to a retired person is

given to the legal heir or heirs after his or her death. For the legal heir or

heirs, this becomes an income and it is taxable under the head 'income from

other sources'. However, the legal heir or heirs can claim a deduction of 33

1/3 % or Rs. 15,000 whichever is lesser according to Section 57 of the Income

Tax Act.

Interest received from investment in securities: While the Income Tax Act does not define a 'security'

specifically, it is generally considered as a secured acknowledgement of a

claim or debt. Central or State Government securities, bonds, and debentures

issued by companies provide interests to the investor. Since the earned

interest is considered as 'income from other sources', it is a taxable income. It

is taxed at 30% (plus 3% cess), irrespective of the individual's tax slab.

There are certain

incomes that do not fall under the four heads of income, which make them

taxable under the head, 'income from other sources'. Interest on loans,

insurance commissions, rent from a vacant land, interest on bank deposits or

deposits with companies are some of the examples of such incomes. They must not

be ignored by any individual while filing the Income Tax Returns.